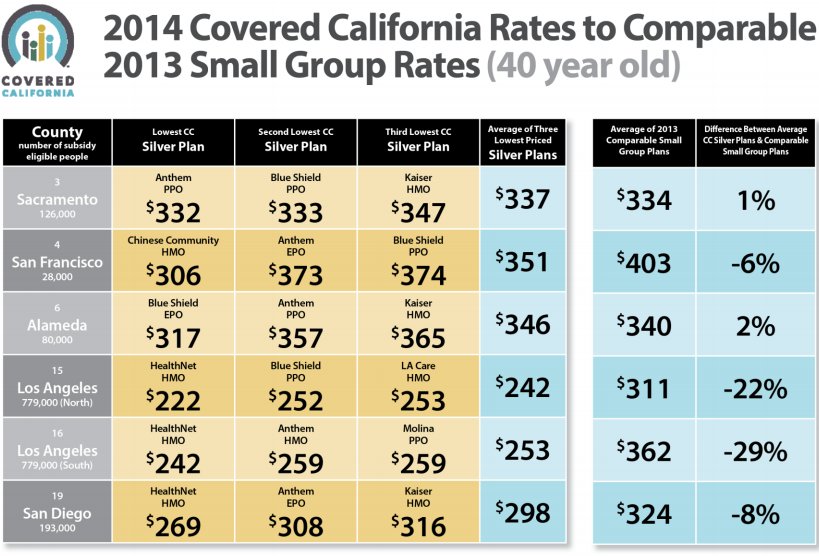

Note Well: The above chart compares 2013 pre-Obamacare private insurance rates with Obamacare's "Silver Plans" which, remarkably, are a full step up from Obamacare's "Bronze Plans."

***

So far, premiums are coming in a bit lower than was anticipated by the Congressional Budget Office, according to a new report. That doesn’t mean Obamacare is cheap, but worries about massive cost spikes may be overblown.

Alan: Prior to Obamacare, insurance companies could -- and did -- refuse to insure people who had pre-existing health problems. Furthermore, anyone who developed a health problem while insured, could (and did) have their coverage cut. It is astonishing -- nay, jaw-dropping -- that Obamacare, which prevents insurance companies from refusing coverage or cutting coverage, is LESS expensive than the status quo ante. Given the flabbergasting, stem-to-stern rip-off that used to be the insurance industry norm, one would expect Obamacare to be several-fold more expensive than erstwhile rates. Instead, Obamacare covers just about everyone -- including every sick person who used to be "locked out" of insurance -- and, generally speaking, provides good coverage at LOWER cost. This is an actual, factual miracle more impressive than Moses parting The Red Sea. Obamacare does not quite bring people back from the dead. But damn near!

Meanwhile, the idiots...

Well... the idiots do what idiots do.

They remain idiots.

In ten years however, they will be manning the barricades to protect Obamacare from austere budget cutters who will still be doing everything in their power to further enrich The 1%.

Meanwhile, the idiots...

Well... the idiots do what idiots do.

They remain idiots.

In ten years however, they will be manning the barricades to protect Obamacare from austere budget cutters who will still be doing everything in their power to further enrich The 1%.

Mark Trumbull

If you live in Florida, Illinois, or Texas, you don’t know yet, even though President Obama’s Affordable Care Act calls for the exchanges to be up and running in less than a month.

That’s one reason the debate over Obamacare’s impact on health insurance costs is still unsettled. Not all the data are in.

But the Kaiser Family Foundation weighed in Thursday with a report on some 17 states, plus the District of Columbia, that have unveiled their pricing.

The report concludes that, from the numbers that are in so far, premiums are coming in a bit lower than was anticipated by the Congressional Budget Office. That doesn’t mean health care under the Obama reforms is cheap, but worries about massive cost spikes may be overblown.

As individuals around the nation prepare for the law’s mandate to have insurance in 2014, or pay a tax penalty, the Kaiser report compiles the states’ figures into comparative tables.

Monthly premiums for a single 40-year-old with an income of $29,000 would be $201 in Portland, Ore., for a typical “silver” plan offered by insurers. In New York City, that same plan would be $390. (Plans are labeled gold, silver, or bronze based on how much the buyer will have to pay out of pocket. A gold plan costs more in premiums but has lower deductibles.)

Now here’s the Obamacare twist: Since the income for that 40-year-old is less than four times the poverty rate, government subsidies will kick in that bring the individual’s cost down to $193 per month in both places. It’s also $193 in Hartford, Conn., and in Los Angeles.

The subsidies, however, phase out entirely for households above four times the poverty level. Those buyers will feel the full impact of price variations – with the New York City insurance shopper owing more than the one inOregon.

“While premiums will vary significantly across the country, they are generally lower than expected,” the authors of the Kaiser report write. “For example, we estimate that the latest projections from the Congressional Budget Office imply that the premium for a 40-year-old in the second lowest cost silver plan would average $320 per month nationally. Fifteen of the eighteen rating areas we examined have premiums below this level….”

The report also indicates that there will be greater consumer choice in some states than in others.

California, Ohio, New York, Oregon, and Colorado will each offer residents a choice among 10 or more insurance providers.

Nebraska, Indiana, Connecticut, and Vermont have fewer than five insurers on their statewide exchanges.

“The current individual insurance market is highly concentrated, with a single insurer dominating at least half the market in 30 states and the District of Columbia,” the report concludes. “That is not likely to change immediately, though the ease of purchasing through exchanges and guaranteed access to coverage regardless of health status should make it easier for consumers to switch plans.”

The report shies away from making comparisons of insurance costs “pre” and “post” Obama reforms. For one thing, the law mandates a whole different approach to insurance in which individuals, for example, can’t be asked to pay sky-high prices because of preexisting medical conditions. (Alan: Nor can Obamacare coverage be denied for any reason, whether pre-existing or manifesting while insured.)

Related stories

No comments:

Post a Comment