Alan: Actually, McConnell is not that bad.

He's worse.

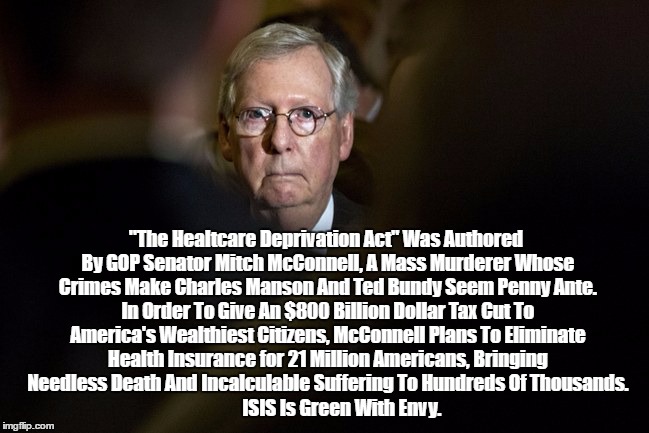

Harvard Study: 45,000 Americans Die Annually For Lack Of Health Insurance

Rep. Joe Kennedy III Tells "Christian" Trump-Care Supporters: Your So-Called "Mercy" Is "Malice"

Rep. Joe Kennedy III Tells "Christian" Trump-Care Supporters: Your So-Called "Mercy" Is "Malice"

The Cruel Old Party: The GOP’s Passage Of Trumpcare Is Unprecedentedly Callous

7 Years' Bitching About Obamacare While Continually Touting Their "Terrific, Low-Cost Replacement" And The GOP Produces Nothing But Flatulence, Excrement And Anguish For 25 Million Americans, Simultaneously Tranferring Hundreds Of Billions Of Dollars To The 1%

Abomicare: Trump's Titanic Failure

What's Missing From This Photo of Politicians Deciding the Future of Women's Health? Anyone?

http://paxonbothhouses.blogspo

Pax On Both Houses: Blog Posts About Canada

Pax On Both Houses: Blog Posts About Canada

(Mostly About Single Payer Healthcare, "Not Perfect, Just Better")

The C.B.O. Gives the Senate Twenty-Two Million Reasons to Reject the Health-Care Bill

In the run-up to the Congressional Budget Office’s release of its study of the Senate Republicans’ health-care reform bill, on Monday afternoon, you could tell that the Trump Administration and its allies on Capitol Hill were getting nervous.

On Sunday, Tom Price, the Secretary of Health and Human Services, took a preëmptive shot at the messenger, claiming, without much basis, that the C.B.O. does a “relatively poor job” of analyzing the number of people who will be insured and uninsured under any given piece of legislation. Also on Sunday, Kellyanne Conway claimed, on ABC News, that the Senate bill wouldn’t cut Medicaid, the federal program that provides health care to poor families, even though the legislation states in black and white that it will roll back the expansion of the program that took effect under the Affordable Care Act.

The Administration’s nervousness turned out to be justified. The C.B.O.’s analysis said that, relative to the current law, the Senate legislation would increase the number of Americans who are uninsured by about twenty-two million people over ten years. This number was very close to the estimate of twenty-three million more uninsured that the same office attached, last month, to the House Republicans’ reform bill—the widely unloved American Health Care Act, which even President Trump subsequently described as “mean.”

The C.B.O., which cherishes its independence and nonpartisan status, doesn’t use words like “mean” or “kind.” It simply lays out its projections, which, in this case, showed that “the increase in the number of uninsured people relative to the number projected under current law would reach 19 million in 2020 and 22 million in 2026. . . . By 2026, among people under age 65, enrollment in Medicaid would fall by about 16 percent and an estimated 49 million people would be uninsured,” compared to twenty-six million today.

The American population as a whole is also projected to expand during the next decade, so the raw numbers perhaps don’t tell the full story. But the C.B.O. analysis also projects a sharp rise in the uninsured rate—the proportion of people under the age of sixty-five who don't have health coverage. After the gains made since the introduction of the Affordable Care Act, that rate in 2017 is down to about ten per cent. If the Senate bill were enacted, the C.B.O. said, this rate would jump to eighteen per cent by 2026, which is about where it was when Barack Obama came to office.

Two factors account for most of the drop in coverage that the C.B.O. projects. In the next two or three years, the biggest impact would come from the abolition of the individual mandate to purchase insurance. Since young and healthy people would no longer face a financial penalty for forgoing coverage, many more of them would probably decide to skip it.

Two factors account for most of the drop in coverage that the C.B.O. projects. In the next two or three years, the biggest impact would come from the abolition of the individual mandate to purchase insurance. Since young and healthy people would no longer face a financial penalty for forgoing coverage, many more of them would probably decide to skip it.

As time went on, the cuts to Medicaid that the legislation contains would start to have a dramatic effect. Over ten years, these cuts would total about seven hundred and seventy billion dollars, the C.B.O. analysis said. By 2021, some ten million fewer people would be enrolled in Medicaid and its sibling, the Children’s Health Insurance Program. By 2025, this number would rise to fifteen million. Indeed, the fall in Medicaid enrollment would account for about two-thirds of the over-all drop in coverage that the C.B.O. projects.

Whatever Trump and the Republicans might say, these figures make it very clear that the working poor would be huge losers under the bill. One of the progressive innovations of the A.C.A.’s expansion of Medicaid was that it allowed working families who subsisted just above the poverty line to get access to health care. According to the Kaiser Family Foundation, about sixty per cent of the people who enrolled in the program were employed. Under the Senate bill (and the House bill), many of these workers, some of whom could be earning as little as fifteen thousand dollars a year, would no longer be eligible for Medicaid in a few years, and they would have to take their chances in the open market.

For them and anybody else who buys individual insurance, the outlook would be grim. The C.B.O. analysis said that premiums in the private market would rise by about twenty per cent next year, on average, because of the elimination of the individual mandate. After that, price premiums would start to fall relative to the current law, but so would the quality of insurance plans. Plans would offer fewer health services, and deductibles would rise even further.

All this would happen by design. Under current law, the benchmark “silver” insurance plan covers about seventy per cent of over-all health-care costs and has a deductible of about thirty-six hundred dollars. Under the Senate plan, beginning in 2020, the benchmark plan would cover about fifty-eight per cent of over-all costs, and it would have a deductible of about six thousand dollars. For many people, that is a small fortune. “As a result,” the C.B.O. report notes dryly, “despite being eligible for premium tax credits, few low-income people would purchase any plan.”

The bad news for purchasers in the individual market doesn’t end there, either. Under the Senate bill, individual states could seek waivers that allow them to duck other provisions of the A.C.A. that were introduced to prevent health costs from bankrupting people with costly diseases, such as diabetes or cancer. As a result of these waivers, the report says, “some enrollees could see large increases in out-of-pocket spending because annual or lifetime limits would be allowed.”

Contrary to expectations in some quarters, the Senate legislation didn't even properly fix one obvious political problem of the House bill: the huge increases in premiums that some elderly people could face. Although the House’s tax credits would be replaced with direct subsidies, a sixty-four-year-old who earns $26,500 a year would see the annual premiums on his silver-level plan rise from $1,700 to $6,500. If he or she earned $56,800 a year, the premiums would jump from $6,800 to $20,500.

And who would be the winners? The very rich, of course. The bill would eliminate the investment tax and income surtax that the A.C.A. imposed on households earning more than a quarter of a million dollars a year. While many poor and middle-income Americans would be adversely affected, these lucky few would get a hefty handout.

For some reason, the White House didn’t mention these winners in its response to the report. Instead, it issued a statement that tried to rubbish the C.B.O.’s insurance-coverage projections. But the C.B.O.’s estimates are the best we have, and for decades both parties have relied on them in assessing prospective legislation. The ineluctable truth is that Senate bill, like the House bill it largely mimics, would have immensely damaging consequences. In pointing this out calmly and clearly, the C.B.O. has performed an invaluable public service.

In the run-up to the Congressional Budget Office’s release of its study of the Senate Republicans’ health-care reform bill, on Monday afternoon, you could tell that the Trump Administration and its allies on Capitol Hill were getting nervous.

On Sunday, Tom Price, the Secretary of Health and Human Services, took a preëmptive shot at the messenger, claiming, without much basis, that the C.B.O. does a “relatively poor job” of analyzing the number of people who will be insured and uninsured under any given piece of legislation. Also on Sunday, Kellyanne Conway claimed, on ABC News, that the Senate bill wouldn’t cut Medicaid, the federal program that provides health care to poor families, even though the legislation states in black and white that it will roll back the expansion of the program that took effect under the Affordable Care Act.

The Administration’s nervousness turned out to be justified. The C.B.O.’s analysis said that, relative to the current law, the Senate legislation would increase the number of Americans who are uninsured by about twenty-two million people over ten years. This number was very close to the estimate of twenty-three million more uninsured that the same office attached, last month, to the House Republicans’ reform bill—the widely unloved American Health Care Act, which even President Trump subsequently described as “mean.”

The C.B.O., which cherishes its independence and nonpartisan status, doesn’t use words like “mean” or “kind.” It simply lays out its projections, which, in this case, showed that “the increase in the number of uninsured people relative to the number projected under current law would reach 19 million in 2020 and 22 million in 2026. . . . By 2026, among people under age 65, enrollment in Medicaid would fall by about 16 percent and an estimated 49 million people would be uninsured,” compared to twenty-six million today.

The American population as a whole is also projected to expand during the next decade, so the raw numbers perhaps don’t tell the full story. But the C.B.O. analysis also projects a sharp rise in the uninsured rate—the proportion of people under the age of sixty-five who don't have health coverage. After the gains made since the introduction of the Affordable Care Act, that rate in 2017 is down to about ten per cent. If the Senate bill were enacted, the C.B.O. said, this rate would jump to eighteen per cent by 2026, which is about where it was when Barack Obama came to office.

Two factors account for most of the drop in coverage that the C.B.O. projects. In the next two or three years, the biggest impact would come from the abolition of the individual mandate to purchase insurance. Since young and healthy people would no longer face a financial penalty for forgoing coverage, many more of them would probably decide to skip it.

As time went on, the cuts to Medicaid that the legislation contains would start to have a dramatic effect. Over ten years, these cuts would total about seven hundred and seventy billion dollars, the C.B.O. analysis said. By 2021, some ten million fewer people would be enrolled in Medicaid and its sibling, the Children’s Health Insurance Program. By 2025, this number would rise to fifteen million. Indeed, the fall in Medicaid enrollment would account for about two-thirds of the over-all drop in coverage that the C.B.O. projects.

Whatever Trump and the Republicans might say, these figures make it very clear that the working poor would be huge losers under the bill. One of the progressive innovations of the A.C.A.’s expansion of Medicaid was that it allowed working families who subsisted just above the poverty line to get access to health care. According to the Kaiser Family Foundation, about sixty per cent of the people who enrolled in the program were employed. Under the Senate bill (and the House bill), many of these workers, some of whom could be earning as little as fifteen thousand dollars a year, would no longer be eligible for Medicaid in a few years, and they would have to take their chances in the open market.

For them and anybody else who buys individual insurance, the outlook would be grim. The C.B.O. analysis said that premiums in the private market would rise by about twenty per cent next year, on average, because of the elimination of the individual mandate. After that, price premiums would start to fall relative to the current law, but so would the quality of insurance plans. Plans would offer fewer health services, and deductibles would rise even further.

All this would happen by design. Under current law, the benchmark “silver” insurance plan covers about seventy per cent of over-all health-care costs and has a deductible of about thirty-six hundred dollars. Under the Senate plan, beginning in 2020, the benchmark plan would cover about fifty-eight per cent of over-all costs, and it would have a deductible of about six thousand dollars. For many people, that is a small fortune. “As a result,” the C.B.O. report notes dryly, “despite being eligible for premium tax credits, few low-income people would purchase any plan.”

The bad news for purchasers in the individual market doesn’t end there, either. Under the Senate bill, individual states could seek waivers that allow them to duck other provisions of the A.C.A. that were introduced to prevent health costs from bankrupting people with costly diseases, such as diabetes or cancer. As a result of these waivers, the report says, “some enrollees could see large increases in out-of-pocket spending because annual or lifetime limits would be allowed.”

Contrary to expectations in some quarters, the Senate legislation didn't even properly fix one obvious political problem of the House bill: the huge increases in premiums that some elderly people could face. Although the House’s tax credits would be replaced with direct subsidies, a sixty-four-year-old who earns $26,500 a year would see the annual premiums on his silver-level plan rise from $1,700 to $6,500. If he or she earned $56,800 a year, the premiums would jump from $6,800 to $20,500.

And who would be the winners? The very rich, of course. The bill would eliminate the investment tax and income surtax that the A.C.A. imposed on households earning more than a quarter of a million dollars a year. While many poor and middle-income Americans would be adversely affected, these lucky few would get a hefty handout.

For some reason, the White House didn’t mention these winners in its response to the report. Instead, it issued a statement that tried to rubbish the C.B.O.’s insurance-coverage projections. But the C.B.O.’s estimates are the best we have, and for decades both parties have relied on them in assessing prospective legislation. The ineluctable truth is that Senate bill, like the House bill it largely mimics, would have immensely damaging consequences. In pointing this out calmly and clearly, the C.B.O. has performed an invaluable public service.

No comments:

Post a Comment