To understand why this cartoon represents standard operating procedure, read

"Noam Chomsky Quotations"

***

"Politics and Economics: The 101 Courses You Wish You Had"

http://paxonbothhouses.blogspot.com/2012/01/politics-and-economics-101-curricula.html

***

"Politics and Economics: The 101 Courses You Wish You Had"

http://paxonbothhouses.blogspot.com/2012/01/politics-and-economics-101-curricula.html

***

***

Just when it seemed that there was nothing more to learn about the illegal and immoral culture which has permeated JP Morgan Chase, the nation’s largest bank, more facts emerge. Its recent Justice Department settlement, which has been oversold as a “$13 billion” agreement, airs some new dirty laundry – and gives us another look at the old stuff.

Here are ten things we learned, or were reminded about, in this latest settlement announcement:

1. JPM defrauded investors on a grand scale.

The Justice Department didn’t work very hard in its review of JPM’s mortgage securities business. But then, it didn’t have to. It’s easy to find evidence of JPM’s crimes.

In her excellent analysis of the settlement for the New York Times, Gretchen Morgensen points out that the DOJ only looked at ten of the bank’s securitizations. An analysis for the Dexia investors’ lawsuit, by contrast, reviewed more than fifty of them. (The Dexia lawsuit is much more informative than the Justice Department’s, and has been publicly available since last year.)

Once again, a lawbreaking bank has not been required to admit guilt as part of a settlement. But the Justice Department’s “Statement of Facts” states its findings fairly plainly:

As discussed below, employees of JPMorgan, Bear Stearns, and WaMu received information that, in certain instances, loans that did not comply with underwriting guidelines were included in the RMBS sold and marketed to investors; however, JPMorgan, Bear Stearns, and WaMu did not disclose this to securitization investors.

The word for that kind of behavior is “fraud.’

2. JPM lied to investors in order to knowingly and willfully defraud them out of billions.

As the Statement of Facts makes clear, employees of JP Morgan Chase were engaged in deliberate and systematic fraud. From the Statement of facts:

JPMorgan employees were informed by due diligence vendors that a number of the loans included in at least some of the loan pools that it purchased and subsequently securitized did not comply with the originators’ underwriting guidelines …

What happened then? You guessed it:

JPMorgan represented to investors in various offering documents that loans in the securitized pools were originated “generally” in conformity with the loan originator’s underwriting guidelines; and that exceptions were made based on “compensating factors,” determined after “careful consideration” on a “case-by-case basis.”

In other words, they knowingly lied in order to cheat investors into thinking these mortgage-backed securities were sound investments – even though they already knew they were terrible.

3. JPM lied to the public.

In that quote, Dimon was attempting to blame homeowners for the poor quality of his bank’s securities. We now know that his own bankers, including senior executives, were responsible. From the DOJ’s Statement of Facts:

Prior to JPMorgan purchasing the loans, a JPMorgan employee who was involved in this particular loan pool acquisition told an Executive Director in charge of due diligence and a Managing Director in trading that due to their poor quality, the loans should not be purchased and should not be securitized. After the purchase of the loan pools, she submitted a letter memorializing her concerns to another Managing Director, which was distributed to other Managing Directors. JPMorgan nonetheless securitized many of the loans. None of this was disclosed to investors.

4. Journalists misled the public, too, probably without even realizing it.

From Lowenstein’s 2010 profile of Dimon:

((Dimon) was adamant that government officials — he seemed to include President Obama — have been unfairly tarring all bankers indiscriminately. “It’s harmful, it’s unfair and it leads to bad policy,” he told me again and again.

That’s not misleading. Lowenstein’s just reporting what Dimon had to say. But this is:

It’s a subject that makes him boil, because Dimon’s career has been all about being discriminating — about weighing this or that particular risk, sifting through the merits of this or that loan.

Using an authoritative tone in an authoritative newspaper, Lowenstein informs us that “Dimon’s career has been all about discriminating” and “weighing … risk.”As we now know from the public record: Er, not so much. And Lowenstein’s just one of dozens who reported on Dimon this way.

Perhaps the best defense these credulous reporters can offer, now that more of the facts are in, came first from Dimon’s lips: “We didn’t anticipate the lying.”

5. JPM said it wasn’t them. It was them.

JPMorgan Chase executives have consisted argued that they’re being punished from fraud committed by the two institutions they acquired with government approval and encouragement, Bear Stearns and Washington Mutual.

But, as the above quotes make clear, JPM’s own bankers behaved as badly as those at these institutions, or worse.

6. Both JPM and the Justice Department have misled the public about the size of this deal.

It’s not really a $13 billion deal. This agreement rolls up a number of independent negotiations, each of which would presumably have led to a settlement of some kind. A $2 billion fine will be paid to the prosecutors’ office in Sacramento. (Without its vigilance, this deal might never have happened.)

Other funds will go to Federal agencies and state attorneys general. The $4 billion set aside for “struggling homeowners” includes loan concessions the bank was already making out of self-interest. (See David Dayen for more on this topic.)

What’s more, most of the settlement will be tax-deductible. Among other things, that means that this deal will deprive the government of funds that are needed for a variety of purposes – including helping the victims of Wall Street fraud.

7. The critics were right.

For years the banking industry and its media defenders have lectured the rest of us, telling us that criticism of Wall Street is unfair, unjust, and tars even the best of the big bankers with the same brush. They always pointed to JPMorgan Chase as the example which proves that not all of America’s megabanks are morally bankrupt.

They can’t say that anymore.

In 2011 Jamie Dimon had some choice words tfor the Occupy movement. “Acting like everyone who’s been successful is bad and that everyone who is rich is bad,” he said. “

Not everybody, Jamie. Just people like you and your colleagues.

8. Jamie Dimon says bankers should “keep to a higher standard.” Now he tells us.

In the wake of yet another brewing JPM scandal over the manipulation of LIBOR rates, Dimon reportedly told his staff that “We all need to keep a higher standard.”

“Don’t exaggerate, don’t ruminate, don’t bulls**t,” Dimon reportedly told his employees. He did not add the words, “That’s my job.”

9. Once again, the criminals are paying the fine with other people’s money.

The fraudsters – and the senior executives who are responsible for keeping their corporation crime-free – won’t be paying this settlement, any more than they’ve paid for any of the many fines and settlements that preceded it.

The money will come from shareholders, many of whom were also deceived about the nature and extent of the bank’s fraud.

You could teach it as Criminal Justice for Schoolkids: If you steal something and don’t have to give it back when you’re caught, you’ll keep right on stealing. That’s something even a first grader can understand, although it’s called “deterrence” in professional circles.

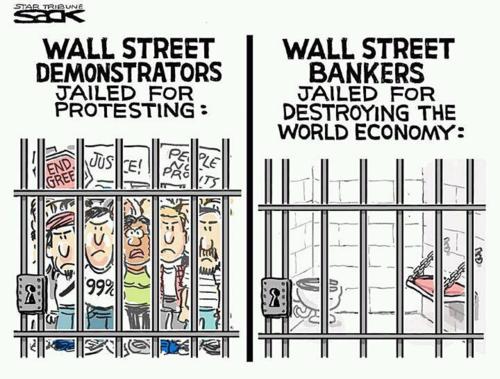

10. Nobody’s going to jail.

And speaking of deterrence:

Until a senior bank executive goes to prison, as more than 800 did after the much smaller savings and loan scandal, things aren’t likely to change very much – at JPMorgan Chase or any other big bank.

ABOUT RICHARD (RJ) ESKOW

Richard (RJ) Eskow is a well-known blogger and writer, a former Wall Street executive, an experienced consultant, and a former musician. He has experience in health insurance and economics, occupational health, benefits, risk management, finance, and information technology.

No comments:

Post a Comment